Against the backdrop of increasingly vibrant M&A activities and corporate restructuring in Vietnam, capital transfer has become a common transaction for both domestic and international investors. These activities are regulated by various provisions across different legal instruments, including: the Law on Enterprises; the Law on Investment; Tax laws including: personal income tax (“PIT”), corporate income tax (“CIT”), and value added tax (“VAT”); the Law on tax administration; and their respective guiding documents.

In practice, the determination of tax obligations and liabilities for capital transfer transactions varies significantly, depending on: (i) the legal status of the transferor; (ii) the legal status of the transferee; (iii) whether the transferred interest constitutes shares (“CS”) or contributed capital (“CC”); and (iv) whether the transaction is a direct or indirect capital transfer.

This article provides a comprehensive yet in-depth overview of tax obligations in capital transfer transactions, enabling investors to proactively manage risks and optimize transaction efficiency.

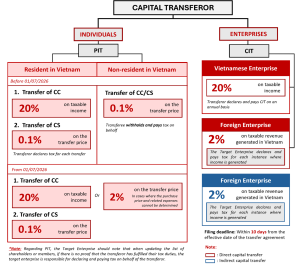

Summary chart of tax obligations in capital transfer transactions

- Capital transfer activities are not subject to VAT

Pursuant to Article 5.9(d) of the Law on VAT 2024, capital transfer activities consist of: “d) Capital transfer including: transfer of part or all of capital invested in another business organization (regardless of establishment of a new juridical person), transfer of securities, transfer of the right to contribute capital and other forms of capital transfer prescribed by law, including selling an enterprise to another enterprise for business operation where the buying enterprise inherits all rights and obligations of the enterprise being sold as prescribed by law. Capital transfer prescribed in this Point does not include transfer of investment projects and sale of assets” which are not subject to VAT.

- PIT/CIT obligations for capital transfer activities

2.1. PIT: applicable where the transferor is an individual.

Summary table of PIT obligations for individual transferors.

Transferor | Basis for tax determination | Tax declaration and payment responsibility | |

Before 01/07/2026[1] | From 01/07/2026[2] | ||

Individuals resident in Vietnam | – Transfer of CC: 20% on taxable income. – Transfer of CS: 0.1% on the transfer price. | – Transfer of CC: o 20% on taxable income. o 2% on the transfer price in cases where the purchase price and related expenses cannot be determined. – Transfer of CS: 0.1% on the transfer price. | – Resident individuals shall declare tax upon each transfer, regardless of whether taxable income is generated [3]. – Deadline for tax declaration and payment: Within 10 days from the effective date of the Transfer Agreement[4]. |

Individuals non-resident in Vietnam | – Transfer of CC/CS: Tax rate of 0.1% on the transfer price | – The transferee shall withhold and declare tax upon each instance where income is generated[5]. – Deadline for tax declaration and payment: Within 10 days from the effective date of the Transfer Agreement[6]. | |

The enterprise whose shares or contributed capital are being transferred (the “Target Enterprise”) must note that during the procedures for changing shareholders or capital contributing members, if there are no supporting documents to prove that the transferring individual has fulfilled their tax obligations, the Target Enterprise shall be responsible for declaring and paying tax on behalf of such individual[7].

Furthermore, it is important to note that if an individual shareholder has previously received distributed dividends, upon transferring those shares, in addition to the PIT on the share transfer, the transferor is also obligated to pay PIT on income from capital investment at a tax rate of 5% on the value of the dividends received.

2.2. CIT: applicable where the transferor is an enterprise.

Transferor | Basis for tax determination | Tax declaration and payment responsibility |

Enterprises established and operating under Vietnamese law. | 20% on taxable income from capital transfer[8]. | The transferring enterprise shall declare and pay CIT on an annual basis[9]. |

Enterprises established and operating under foreign law (except for intra-group ownership restructuring as presented in Section 5 below). | 2% on taxable revenue generated in Vietnam[10]. | – The transferee, being an enterprise established and operating under Vietnamese law, shall be responsible for paying tax on behalf of the transferor[11]. – The Target Enterprise shall be responsible for paying tax on behalf of the transferor if the transferee is also a foreign organization or individual[12]. – Tax shall be declared and paid upon each instance where income is generated[13]. – Deadline for tax declaration and payment: Within 10 days from the effective date of the Transfer Agreement[14]. |

Key Considerations:

- In the event that an owner enterprise sells its entire capital interest in a single-member limited liability company (LLC) whose sole primary asset is real estate, CIT shall be declared and paid in accordance with regulations governing real estate transfer activities;

- Where a capital transfer is settled through non-monetary consideration (including shares, fund certificates, or other material benefits) resulting in income, such income is subject to CIT. The value of assets, shares, fund certificates, and other material benefits shall be determined based on the market selling price at the time of receipt;

- In cases where the transfer agreement provides for payment via installments or deferred payment, the transfer revenue shall exclude interest on installments or deferred payment as stipulated in the agreement;

- Enterprises executing transfer transactions with a value of 5 million VND or more must possess non-cash payment instruments. In the absence of such non-cash payment instruments, the tax authorities reserve the right to assess the transfer price.

- Transfer expenses are actual costs directly related to the transfer, supported by legitimate invoices and vouchers, including:

- Costs incurred for necessary legal procedures regarding the transfer;

- Fees and charges payable during the transfer process;

- Expenses for transaction, negotiation, and execution of the transfer agreement, and other documented costs;

- Where transfer expenses are incurred overseas, the original vouchers must be certified by a notary public or an independent auditing firm in the country of origin. Such vouchers must be translated into Vietnamese and certified by a competent representative.

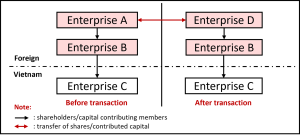

- Indirect capital transfer

Pursuant to the Law on CIT 2025 and its guiding documents, foreign enterprises—including those with or without a Permanent Establishment (PE) in Vietnam—are obligated to pay tax on taxable income arising in Vietnam. This includes income from capital transfers in Vietnam, whether through direct or indirect transfer, regardless of the location where the transfer is executed[15]. In cases where the transferee of a foreign enterprise’s capital is also a foreign organization or individual, the taxpayer shall be the enterprise established under Vietnamese law in which the foreign organizations have invested their capital[16].

(Diagram illustrating an indirect capital transfer)

In the above diagram, the transfer of capital interests in Enterprise B from Enterprise A to Enterprise D, despite Enterprise B, Enterprise D, and the transaction itself being located entirely offshore, indirectly results in a change of ownership within Enterprise C in Vietnam. In this case, Enterprise C in Vietnam is obligated to declare and pay tax on the capital transfer transaction between Enterprise A and Enterprise D, at a tax rate of 2% on the taxable revenue generated in Vietnam[17].

- Regulations on intra-group ownership restructuring

According to current regulations, foreign enterprises engaging in capital transfers as part of intra-group ownership restructuring—which do not result in a change of the ultimate parent company of the participating parties with direct or indirect ownership of the Vietnamese enterprise after restructuring, and where no income is generated—shall not be subject to CIT in Vietnam[18].

Specifically, ownership restructuring transactions include: demergers (separation, split-off); consolidations; mergers; share swaps; capital contributions by shares; distribution of profits or dividends in the form of shares within the group; and other transactions involving the direct or indirect movement of ownership in a Vietnamese enterprise.

Such transactions must simultaneously satisfy the following conditions:

- No change in the ultimate beneficial owner;

- The transfer value is not recorded higher than the book value or the initial contributed capital value; the transaction does not create a price difference; the value determined according to the restructuring dossier approved by competent authorities is not higher than the value recorded at the time of the capital transfer;

- The transferee inherits the entire capital value, as well as all obligations and rights related to the investment of the transferor.

- Applying double taxation avoidance agreements between Vietnam and other countries

For organizations and individuals that are tax residents of a country that has signed a double taxation avoidance agreement with Vietnam, when a tax obligation arises from a capital transfer transaction in a Vietnamese business, it is important to consider whether it falls under the case of applying the agreement or not. This is to perform the procedures to apply the agreement and ensure the best tax benefits for income earned in Vietnam.

Additionally, please note that many current Double Taxation Avoidance Agreements between Vietnam and other countries have a rule: Vietnam has the right to collect income tax if a foreign party transfers capital in a business residing in Vietnam where the value of real estate makes up the main part of that business’s total assets. This “main part” is usually defined as over 50%. In this case, the organization or individual resident in the country that signed the agreement with Vietnam is obligated to pay tax in Vietnam and is not eligible for tax exemption under the agreement for income from capital transfers earned in Vietnam.

[1] Article 28 Law on PIT 2007.

[2] Article 13 and Article 23 Law on PIT 2025.

[3] Article 26.4(a) Circular No. 111/2013/TT-BTC of the Ministry of Finance dated 15 August 2013, on the implementation of the Law on PIT, the Law on the amendments to the Law on PIT, and Decree No. 65/2013/NĐ-CP elaborating a number of articles of the Law on PIT and the Law on the amendments to the Law on PIT (“Circular 111/2013”).

[4] Article 44.3 Law on tax administration 2019.

[5] Article 26.4(b) Circular 111/2013.

[6] Article 44.3 Law on tax administration 2019.

[7] Article 7.5(h) Decree No. 126/2020/ND-CP of the Government dated 19 October 2020 on elaboration of the Law on tax administration (“Decree 126”) and Article 26.4(c) Circular 111/2013.

[8] Article 11 and Article 23.9(a) Decree 320 of the Government dated 15 December 2025 on elaboration of some articles and measures for organization, provision of guidelines for implementation of the Law on corporate income tax (“Decree 320”).

[9] Article 13.1(c) Decree 320.

[10] Article 12.3(i) Decree 320.

[11] Article 2.2 Decree 320.

[12] Article 2.2 Decree 320.

[13] Article 8.4(o) Decree 126.

[14] Article 44.3 Law on tax administration 2019.

[15] Article 2 and Article 3, Law on CIT 2025 and Article 3.4 Decree 320.

[16] Article 2.2 Decree 320.

[17] Article 12.3(i) Decree 320.

[18] Article 7.2(m), Circular No. 20/2026/TT-BTC of the Ministry of Finance dated 12 March 2026 on elaboration of the Law on CIT and Decree 320.

Disclaimer: This article is prepared by PTN Legal LLC (“PTN Legal”) solely for the purpose of providing reference information to readers. PTN Legal does not commit to or guarantee the accuracy or completeness of this information. The content of the article may be amended, adjusted, or updated without prior notice. PTN Legal shall not be liable for any errors or omissions in this article or for any damages arising from its use in any circumstances.