As of 1 January 2026, when the Law on Digital Technology Industry (“DTI Law”) came into effect, Vietnam officially became the 46th country to legalize crypto assets. According to VnEconomy, there are currently around 17 million Vietnamese people owning crypto assets. As of 2025, Vietnam ranked among the top 7 countries with the largest number of crypto-asset holders worldwide[1]. With the introduction of the DTI Law, for the first time, Vietnamese legislation recognizes the concepts of “digital assets” and “crypto assets”. Subsequently, Resolution No. 05/2025/NQ-CP of the Government dated 9 September 2025 (“Resolution 05”) established a pilot mechanism for the crypto-asset market for a period of five years. After the pilot period ends, the crypto-asset market will continue to operate under this Resolution until it is amended, supplemented, or replaced by new legal regulations.

These policies reflect a significant shift in the regulatory approach: from caution to proactive, controlled experimentation through a licensed market model with centralized supervision. According to the Government’s plan, crypto-asset trading market are expected to be piloted from the Quarter III of 2026, following the completion of the review and supplementation of relevant mechanisms and legal regulations.

This article analyzes how the crypto-asset market is designed and operated in Vietnam, including market structure, issuance mechanisms, trading activities, and applicable tax obligations.

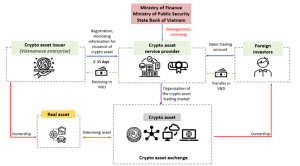

The offering and issuance of crypto assets transaction is outlined in the diagram below:

- Legal Framework Governing Crypto Assets

Under the DTI Law, digital assets are defined as “assets as defined under the Civil Code, expressed in the form of digital data, and created, issued, stored, transferred, and authenticated by digital technologies within an electronic environment”[2].

Digital assets may include[3]: (i) Virtual assets, which are a type of digital asset used for exchange or investment purposes and do not include securities or digital forms of fiat currency[4]; (ii) Crypto assets, which are a type of digital asset that use cryptographic or equivalent digital technologies for authentication during their creation, issuance, storage, and transfer, and are issued based on underlying real assets[5], excluding securities and digital forms of fiat currency[6]; and (iii) Other types of digital assets.

Currently, Vietnamese law provides detailed regulations specifically on crypto assets mainly under Resolution 05 and its implementing instruments, including: (i) Decision No. 96/QD-BTC dated 20 January 2026 of the Ministry of Finance on the promulgation of newly issued administrative procedures for the pilot implementation of the crypto-asset market under its management authority; (ii) Circular No. 15/2026/TT-BTC dated 4 March 2026, guiding accounting principles applicable to entities participating in the crypto-asset market in Vietnam; (iii) Circular No. 32/2026/TT-BTC dated 27 March 2026, providing guidance on tax policies applicable to trading, transfer, and business activities related to crypto assets (“Circular 32”); and (iv) Circular No. 41/2026/TT-BTC dated 6 April 2026, guiding tax declaration, withholding, payment, and finalization in the crypto-asset market (“Circular 41”), applicable during the pilot period.

- Participants in the Crypto Assets Market

The crypto-asset market in Vietnam is structured around the following key groups of participants:

2.1. State regulatory authorities include the Ministry of Finance, the State Bank of Vietnam, and the Ministry of Public Security. These authorities are responsible for licensing, supervision, and management of capital flows, as specifically provided under Article 17 of Resolution 05.

2.2. Crypto-asset service providers are enterprises that carry out one or more of the following activities[7]: (i) organization crypto-asset trading market; (ii) proprietary trading of crypto assets; (iii) custody of crypto assets; and (iv) provision of a crypto asset issuance platform.

Currently, the Ministry of Finance is reviewing applications for licenses for several crypto-asset service providers, thereby laying the foundation for the establishment of an official intermediary system for the market. According to public information, the Ministry of Finance has sent official letters to the Ministry of Public Security and the State Bank of Vietnam to seek opinions on 5 applications for licenses to provide services for organizing crypto-asset trading markets, including: VIX Crypto Assets Exchange Joint Stock Company; Loc Phat Vietnam Crypto Assets Exchange Joint Stock Company (LPEX); Vietnam Prosperity Crypto Assets Exchange Joint Stock Company (CAEX); Techcom Crypto Assets Exchange Joint Stock Company (TCEX); and Vietnam Digital Assets Joint Stock Company[8].

2.3. Crypto-asset issuers are Vietnamese enterprises established as limited liability companies or joint stock companies under the Law on Enterprises, which conduct the offering and issuance of crypto assets to the market[9].

2.4. Investors include both organizations and individuals, comprising[10]: (i) foreign investors; and (ii) domestic investors.

- Regulations on Crypto-Asset Transactions

3.1. Conditions for Offering and Issuance of Crypto Assets

The offering and issuance of crypto assets must satisfy the following conditions:

- Participation is restricted to foreign investors only[11];

- Must be conducted through crypto-asset service providers licensed by the Ministry of Finance[12]; and

- At least 15 days prior to the offering or issuance, the crypto-asset issuer must disclose information in the form of a prospectus, in accordance with the template provided in Appendix I of Resolution 05, on the websites of both the issuer and the licensed crypto-asset service provider[13].

3.2. Trading Through Licensed Crypto-Asset Service Provider

Although the offering and issuance of crypto assets are limited to foreign investors, Resolution 05 still allows domestic investors who already hold crypto assets, as well as foreign investors, to open trading accounts with licensed crypto-asset service providers to conduct trading activities in Vietnam[14].

If, after six months from the date the first crypto-asset service provider is licensed, domestic investors fail to bring their previously held crypto assets into trading through licensed service providers, they may be subject to administrative penalties or criminal prosecution[15]. Currently, the Ministry of Finance is in the process of drafting and consulting on a decree on administrative sanctions in the crypto-asset sector and crypto-asset market. Under the draft decree, the maximum fine is VND 200 million for organizations and VND 100 million for individuals for each violation[16].

For foreign investors, Resolution 05 requires that investment capital inflows and outflows be conducted through a Vietnamese-dong-denominated payment account opened at a bank licensed to provide foreign exchange services in Vietnam[17]. The account-servicing bank is responsible for submitting quarterly reports to the Ministry of Finance, the Ministry of Public Security, and the State Bank of Vietnam on inflows and outflows related to crypto-asset trading transactions conducted by foreign investors[18].

- Tax Policies Applicable to Crypto-Asset Transactions

In order to implement the pilot crypto-asset market in Vietnam, the Ministry of Finance has issued Circular 32 and Circular 41. These circulars take effect from their dates of issuance and remain applicable throughout the pilot period of the crypto-asset market in Vietnam or until new tax policies are introduced. Accordingly, tax obligations arising from trading, transfer, and business activities involving crypto assets in Vietnam are the responsibility of organizations and individuals participating in the crypto-asset market[19], with several notable points as follows:

4.1. The transfer and trading of crypto assets are not subject to value-added tax[20].

4.2. Enterprises providing crypto-asset services are subject to a corporate income tax (“CIT”) rate of 20% on income derived from such services, except where (i) a reduced tax rate of 15% applies to enterprises with total annual revenue not exceeding VND 3 billion; or (ii) a reduced tax rate of 17% applies to enterprises with total annual revenue exceeding VND 3 billion but not exceeding VND 50 billion. The declaration and payment of CIT shall comply with prevailing regulations[21].

4.3. CIT, personal income tax applicable to income derived from the transfer of crypto assets:

Taxpayer | Tax basis | Tax declaration and payment responsibility |

Domestic investors (organizations) | 20% of taxable income (except where a preferential tax rate of 15% applies to entities with total annual revenue not exceeding VND 3 billion, or 17% for revenue exceeding VND 3 billion but not exceeding VND 50 billion) [22]. | Investors shall declare and pay CIT in the same manner as enterprises under prevailing regulations[23]. |

Foreign investors (organizations) | 0.1% on gross proceeds from each transfer transaction[24]. | The crypto-asset service provider is responsible for withholding and remitting tax on behalf of the investor for each crypto-asset transfer conducted through the service provider[25]. Withholding time: at the time the crypto assets transfer transaction is confirmed as successful. Filing and payment deadline: on a monthly basis, no later than the 20th day of the month following the month in which the tax liability arises. |

Individual investors (including both resident and non-resident individuals) | 0.1% on the transfer price per transaction[26]. |

[1] https://vneconomy.vn/viet-nam-la-quoc-gia-thu-46-hop-phap-hoa-tai-san-ma-hoa.htm.

[2] Article 46 DTI Law.

[3] Article 47.1 DTI Law.

[4] Article 47.2(a) DTI Law.

[5] Article 5.2 Resolution 05.

[6] Article 47.2(b) DTI Law and Article 3.2 Resolution 05.

[7] Article 3.3 Resolution 05.

[8] https://vneconomy.vn/5-ho-so-xin-lap-san-giao-dich-tai-san-ma-hoa-hop-le-dang-duoc-lay-y-kien.htm.

[9] Article 3.4 and 5.1 Resolution 05.

[10] Article 3.8 and 3.9 Resolution 05.

[11] Article 6.1 Resolution 05.

[12] Article 7.3 Resolution 05.

[13] Article 6.3 Resolution 05.

[14] Article 7.1 and Article 7.3 Resolution 05.

[15] Article 7.2 Resolution 05.

[16]https://vibonline.com.vn/du_thao/du-thao-nghi-dinh-quy-dinh-xu-phat-vi-pham-hanh-chinh-trong-linh-vuc-tai-san-ma-hoa-va-thi-truong-tai-san-ma-hoa.

[17] Article 13.1 Resolution 05.

[18] Article 13.9 Resolution 05.

[19] Article 14.5 and Article 15.2 Resolution 05.

[20] Article 3.1 Circular 32.

[21] Article 4.2 Circular 32.

[22] Article 4.1 Circular 32.

[23] Article 3.2 and Article 3.3 Circular 41.

[24] Article 4.3 Circular 32.

[25] Article 4 Circular 41.

[26] Article 5 Circular 32.

Disclaimer: This article is prepared by PTN Legal LLC (“PTN Legal”) solely for the purpose of providing reference information to readers. PTN Legal does not commit to or guarantee the accuracy or completeness of this information. The content of the article may be amended, adjusted, or updated without prior notice. PTN Legal shall not be liable for any errors or omissions in this article or for any damages arising from its use in any circumstances.